From the Analysts

|

PIN Debit Acceptance:

|

Over the past few years, offline debit (also known as check card) transaction volume has grown rapidly, to the point where it exceeds that of its older PIN-based debit cousin (also known as online debit). Check card volume grew rapidly over the 1990s due to its advantages of a pre-existing base of accepting merchants and heavy promotion by financial institution issuers. In contrast, PIN-based debit's only major advantage over check cards has been its lower cost to merchants, a difference which has helped earn it a devoted acceptance base among low-margin merchant segments like grocery and petroleum.

Analysts Graph #1

That advantage may be narrowing, however. Visa, for example, recently announced a significant increase in the interchange rate for Interlink, the association's PIN-based debit brand. PIN-based interchange rates, long at low rates to promote merchant acceptance, have been creeping up over the past few years (see graph #1). Continued upward pressure on PIN-debit interchange rates is likely to come from the financial institution owners of many ATM/debit networks, as well as from market pressure on those networks held by public companies.

It is not surprising that Visa, in particular, increased on-line debit interchange. Under pressure from major U.S. retailers to reduce the difference between offline (check card) interchange and PIN-debit pricing, Visa elected to raise its online debit rate rather than lower check card fees. This move may indeed spur a general industry movement to higher PIN-debit interchange. Merchants stand to bear the heightened cost of PIN-debit, as most acquiring contracts are structured to pass through interchange and network fee increases to the retailer.

Regardless of the rising cost to merchants, we expect strong PIN-debit growth to continue. Even at the increased price, merchants and acquirers should still be looking to add PIN-debit to their payment acceptance alternatives for a number of reasons:

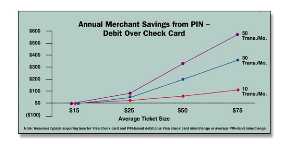

Analysts Graph #2

Analysts Graph #2

The per transaction cost of accepting a PIN-debit transaction is still much lower than the cost of check card (see graph #2). The price difference is even greater than that depicted if one considers the fewer number of chargebacks and reduced fraud associated with PIN-debit.

The per transaction cost of accepting a PIN-debit transaction is still much lower than the cost of check card (see graph #2). The price difference is even greater than that depicted if one considers the fewer number of chargebacks and reduced fraud associated with PIN-debit.

There are indications that consumer preference for PIN-debit over check card is increasing.1

Research performed by First Annapolis indicates that even in traditional PIN-debit segments, many merchants do not yet accept the product. For example, in a survey of over 10,000 U.S merchants completed late last year, we found that over 70% of grocery merchants and over 30% of petroleum merchants still do not accept PIN-debit2.

Upcoming nationwide mandatory rollout of EBT (electronic benefits transfer) will provide an excellent opportunity to piggyback PIN-based debit acceptance.

In summary, acquirers and networks still have a significant opportunity for expanding PIN-debit. Both merchants and consumers benefit from lower costs and reduced risk, consumers seem to prefer the product to its check card alternative and the many likely merchant candidates who have not yet added PIN-debit could be a strong source of revenue growth for ISOs.

Lee Modesitt is a Senior Consultant at Linthicum, MD, based First Annapolis Consulting, Inc., in the electronic banking practice area.

Sources:

1 Star Network survey results announced July 17, 2001.

2 Figures reflect acceptance by unique grocery stores/chains rather than by outlet. Virtually all national chains surveyed accepted PIN-debit.